ICE Market Trend 2025

India 2025 Fuel Mix Shift

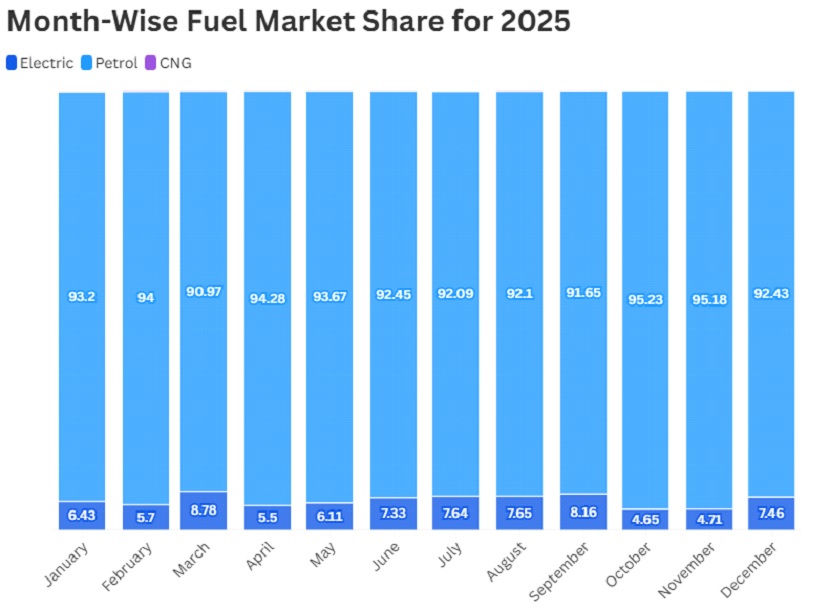

Petrol Dominance with Emerging Electric Momentum India’s two-wheeler fuel mix in 2025 highlights a strong dominance of petrol vehicles across all months, consistently holding above 90% market share. However, a closer look reveals a gradual yet meaningful shift toward electric adoption. Electric vehicles show peaks in March (8.78%) and September (8.16%), indicating rising consumer interest driven by festive demand cycles, regional incentives, and increasing EV awareness across urban and semi-urban markets. Meanwhile, petrol share slightly softens during these periods, reflecting early signs of transition rather than disruption.

CNG continues to remain a niche segment with minimal contribution, steadily declining toward the end of the year. Notably, October and November witness a sharp rebound in petrol share (above 95%), suggesting temporary demand consolidation, possibly influenced by pricing, supply, or seasonal buying behaviour. Overall, the trend indicates a petrol-led market with a gradually strengthening electric footprint, signalling a slow but steady transition in India’s two-wheeler ecosystem driven by evolving consumer preferences and infrastructure growth.

| 2025 | Electric | Petrol | CNG |

|---|---|---|---|

| January | 6.43% | 93.19% | 0.37% |

| February | 5.70% | 94.00% | 0.30% |

| March | 8.78% | 90.97% | 0.25% |

| April | 5.50% | 94.28% | 0.22% |

| May | 6.11% | 93.67% | 0.22% |

| June | 7.33% | 92.45% | 0.22% |

| July | 7.64% | 92.08% | 0.27% |

| August | 7.65% | 92.10% | 0.25% |

| September | 8.16% | 91.65% | 0.19% |

| October | 4.65% | 95.23% | 0.12% |

| November | 4.71% | 95.19% | 0.11% |

| December | 7.46% | 92.43% | 0.11% |

India 2025 ICE Segment Trends: Motorcycle-Led Growth with Seasonal Demand Surges

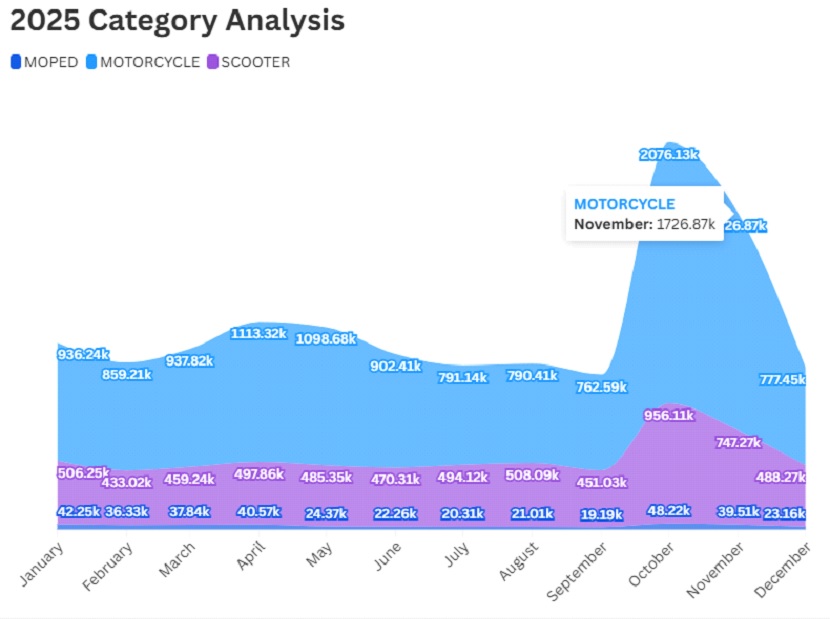

The 2025 ICE (petrol) two-wheeler market in India is strongly driven by motorcycles, consistently contributing the largest share across all months. Motorcycles peak significantly in April (1113k) and show an exceptional surge in October (2076k), highlighting strong festive and seasonal demand patterns across the country. Scooters maintain a stable second position, with relatively consistent volumes throughout the year and a sharp rise during October (956k) and November (747k), indicating increased urban and family-oriented demand during festive periods. Mopeds, on the other hand, remain a smaller but steady segment, with occasional spikes such as October (48k).

A clear trend emerges with mid-year softness (June–September), where all categories witness a dip, likely due to seasonal slowdowns and monsoon impact across key regions. However, the market rebounds strongly in the festive quarter (October–November), driving peak volumes across all segments. Overall, the ICE market remains highly seasonal and motorcycle-dominated, with scooters gaining steady traction and mopeds serving niche, price-sensitive markets across India.

| ICE Month Wise 2025 Analysis | Moped | Motorcycle | Scooter |

|---|---|---|---|

| January | 42.25k | 936.24k | 506.25k |

| February | 36.33k | 859.21k | 433.02k |

| March | 37.84k | 937.82k | 459.24k |

| April | 40.57k | 1113.32k | 497.86k |

| May | 24.37k | 1098.68k | 485.35k |

| June | 22.26k | 902.41k | 470.31k |

| July | 20.31k | 791.14k | 494.12k |

| August | 21.01k | 790.41k | 508.09k |

| September | 19.19k | 762.59k | 451.03k |

| October | 48.22k | 2076.13k | 956.11k |

| November | 39.51k | 1726.87k | 747.27k |

| December | 23.16k | 777.45k | 488.27k |

India 2025 Premium Motorcycle Market (250cc+): Royal Enfield Leads the Segment

In 2025, India’s premium motorcycle segment (250cc+) is clearly dominated by Royal Enfield, maintaining a strong lead across the top five states. Uttar Pradesh stands out as the largest contributor (154k), followed by Maharashtra (106k) and West Bengal (90k), indicating high demand in both mass and emerging premium markets. This trend reflects a strong shift in consumer preference toward higher-displacement motorcycles, especially in aspirational and semi-urban regions.

Other brands like Triumph and KTM are gaining traction in key urban states such as Maharashtra, Karnataka, and Tamil Nadu, showcasing rising demand for performance-oriented and premium bikes. Honda and Bajaj maintain a steady but smaller presence across these regions. Southern markets display relatively diversified brand competition, especially for KTM and Triumph. Overall, the 2025 trend highlights a growing premiumization of the Indian two-wheeler market, led by Royal Enfield, with increasing participation from global and performance-focused brands.

| State (Top 5) | Royal Enfield | Honda | Triumph | KTM | Bajaj |

|---|---|---|---|---|---|

| Uttar Pradesh | 154.48k | 1.88k | 1.38k | 1.1k | 2.2k |

| Maharashtra | 106k | 8k | 10k | 5.73k | 3.59k |

| West Bengal | 90k | 4k | 2k | 4.27k | 4.46k |

| Tamil Nadu | 75k | 6k | 6k | 8.97k | 2.13k |

| Karnataka | 64k | 7k | 9k | 7.75k | 2.94k |

Top 10 Cities Driving Premium Motorcycles (250cc+) in India – 2025

The strong demand for premium motorcycles in leading cities such as Bengaluru, Delhi, Mumbai, and Pune is primarily driven by higher disposable incomes, evolving urban lifestyles, and a growing inclination toward performance and aspirational mobility. These markets benefit from well-developed infrastructure, greater accessibility to premium dealerships, and a mature consumer base that values brand, design, and riding experience.

In emerging cities like Patna, Lucknow, and Bhubaneswar, the growth is fueled by rising aspirations, improving economic conditions, and increased exposure to premium brands through digital platforms. Enhanced financing options and expanding dealer networks are further enabling consumers to upgrade to higher-displacement motorcycles. This shift reflects a broader trend of premiumization, extending beyond metros into fast-growing urban centers across India.

| Top 10 Cities | Volumes Motorcycle 2025 |

|---|---|

| Bengaluru | 50.25k |

| Delhi | 50.01k |

| Pune | 20.72k |

| Mumbai | 19.21k |

| Patna | 15.84k |

| Chennai | 14.86k |

| Lucknow | 12.99k |

| Pimpri Chinchwad | 12.67k |

| Ahmedabad | 11.69k |

| Bhubaneswar | 11.63k |

Mid-Segment Scooters Dominate the Market Shift

In 2025, the ICE scooter market in India is clearly shifting toward the 125–150cc segment, which leads with a dominant 52.37% share, reflecting rising consumer preference for better performance and efficiency. The 100–125cc segment remains strong at 46.94%, indicating continued demand in the entry-level space. Higher CC segments above 150cc contribute negligibly, highlighting a clear market concentration in mid-range scooters driven by practicality and value.

| CC | Scooter ICE 2025 |

|---|---|

| 125-150 | 52.37% |

| 100-125 | 46.94% |

| 150-175 | 0.65% |

| 175-200 | 0.03% |

Entry-Level Motorcycles Lead, Premium Gaining Ground

In 2025, India’s ICE motorcycle market is largely driven by the 100–200cc segment, commanding a dominant 50.58% share, followed by sub-100cc bikes at 37.05%, reflecting strong demand for affordability and daily commuting. However, premium segments (300cc and above) are gradually gaining traction, led by the 300–400cc category (8.73%). This indicates a clear shift toward performance-oriented motorcycles alongside a still dominant mass-market base.

| CC | Motorcycle ICE 2025 |

|---|---|

| 100-200 | 50.58% |

| <100 | 37.05% |

| 300-400 | 8.73% |

| 200-300 | 2.50% |

| 400-500 | 0.78% |

| 600-700 | 0.36% |

India 2025 Top ICE Scooter Models: Trust, Utility & Youth Appeal Drive Demand

The 2025 ICE scooter market in India is led by high-trust, mass-market models like Activa and Jupiter, driven by reliability, fuel efficiency, and extensive service networks. These models dominate due to their strong appeal among daily commuters and family users, offering practicality, low maintenance, and consistent performance across urban and semi-urban markets.

At the same time, models like Ntorq, Burgman Street, and Ray ZR highlight a growing shift toward style, performance, and feature-rich scooters, especially among younger buyers. The presence of multiple brands in the top 10 reflects a balanced market where both utility-driven and aspirational products coexist, supported by strong dealership reach, financing accessibility, and brand loyalty across India.

| MAKE | MODEL | SCOOTER 2025 VOLUMES |

|---|---|---|

| HONDA | ACTIVA | 24.68 lacs |

| TVS | JUPITER | 14.11 lacs |

| SUZUKI | ACCESS | 7.85 lacs |

| TVS | NTORQ | 3.3 lacs |

| HONDA | DIO | 2.93 lacs |

| SUZUKI | BURGMAN STREET | 2.87 lacs |

| YAMAHA | RAY ZR | 2.13 lacs |

| HERO | DESTINI | 1.86 lacs |

| HERO | PLEASURE PLUS | 1.4 lacs |

| TVS | ZEST | 1.12 lacs |

India 2025 Top ICE Motorcycles: Mass Leaders with Rising Premium Appeal

The 2025 ICE motorcycle market in India is dominated by high-volume, commuter-focused models like Splendor Plus, HF, Shine, and Platina, driven by affordability, fuel efficiency, and strong rural and semi-urban demand. These models continue to lead due to their reliability, low maintenance, and extensive service networks, making them the backbone of India’s two-wheeler market.

At the same time, models like Pulsar, Apache, and Raider reflect growing demand for sporty, performance-oriented motorcycles among younger consumers. The presence of Royal Enfield Classic highlights the rising premiumization trend, where aspirational and lifestyle-driven purchases are increasing alongside the mass commuter segment.

| MAKE | MODEL | MOTORCYCLE 2025 VOLUMES |

|---|---|---|

| HERO | SPLENDOR PLUS | 34.76 lacs |

| BAJAJ | PULSAR | 13.13 lacs |

| HONDA | SP | 11.26 lacs |

| HERO | HF | 10.14 lacs |

| HONDA | SHINE | 8.65 lacs |

| TVS | APACHE | 5.58 lacs |

| TVS | RAIDER | 4.25 lacs |

| BAJAJ | PLATINA | 4.14 lacs |

| ROYAL-ENFIELD | CLASSIC | 3.91 lacs |

| HONDA | UNICORN | 3.54 lacs |

Electric Market Trend 2025

EV Adoption Gaining Momentum Across Key Indian States – 2025

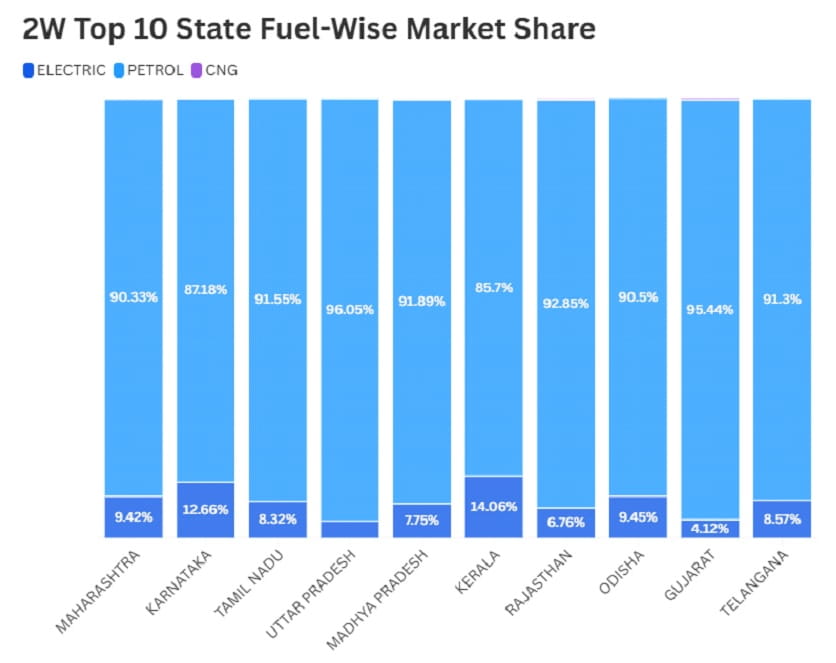

In 2025, electric vehicle (EV) adoption across India’s top states reflects a gradual but uneven transition from petrol dominance. States like Kerala (14.06%) and Karnataka (12.66%) lead in EV penetration, driven by stronger policy support, urbanization, and better charging infrastructure. Maharashtra and Odisha also show healthy adoption levels (~9%), indicating growing acceptance in both western and eastern regions.

However, large markets like Uttar Pradesh (3.82%) and Gujarat (4.12%) continue to be heavily petrol-driven, highlighting slower EV adoption due to infrastructure gaps and price sensitivity. Overall, while petrol remains dominant across all states, the steady rise in EV share signals increasing consumer awareness, supportive state policies, and a clear long-term shift toward electrification in India’s two-wheeler market.

| TOP 10 STATES | ELECTRIC | PETROL | CNG |

|---|---|---|---|

| MAHARASHTRA | 9.42% | 90.33% | 0.25% |

| KARNATAKA | 12.66% | 87.18% | 0.16% |

| TAMIL NADU | 8.32% | 91.55% | 0.13% |

| UTTAR PRADESH | 3.82% | 96.05% | 0.14% |

| MADHYA PRADESH | 7.75% | 91.89% | 0.36% |

| KERALA | 14.06% | 85.70% | 0.24% |

| RAJASTHAN | 6.76% | 92.85% | 0.39% |

| ODISHA | 9.45% | 90.50% | 0.05% |

| GUJARAT | 4.12% | 95.44% | 0.44% |

| TELANGANA | 8.57% | 91.30% | 0.14% |

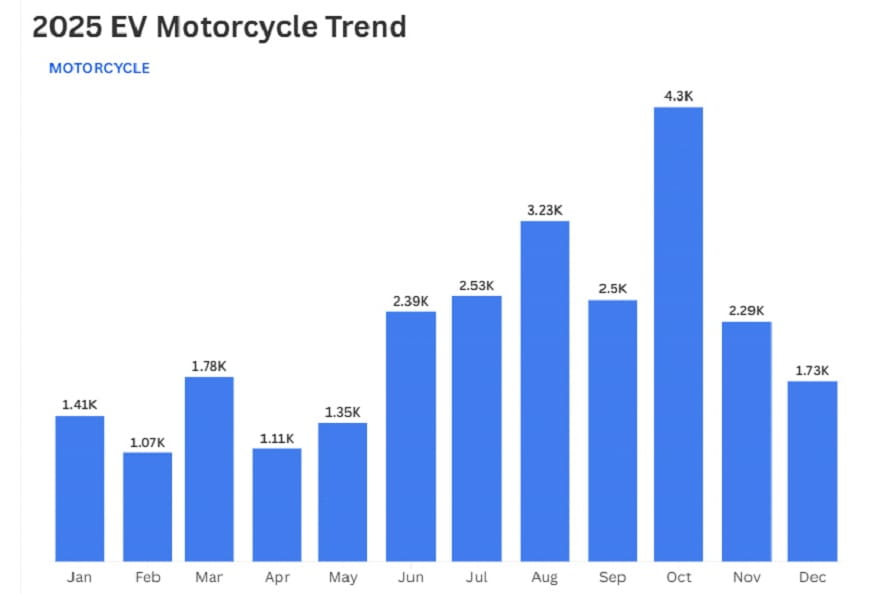

India EV Two-Wheeler Market 2025: Scooter-Led Growth with Emerging Motorcycle Segment

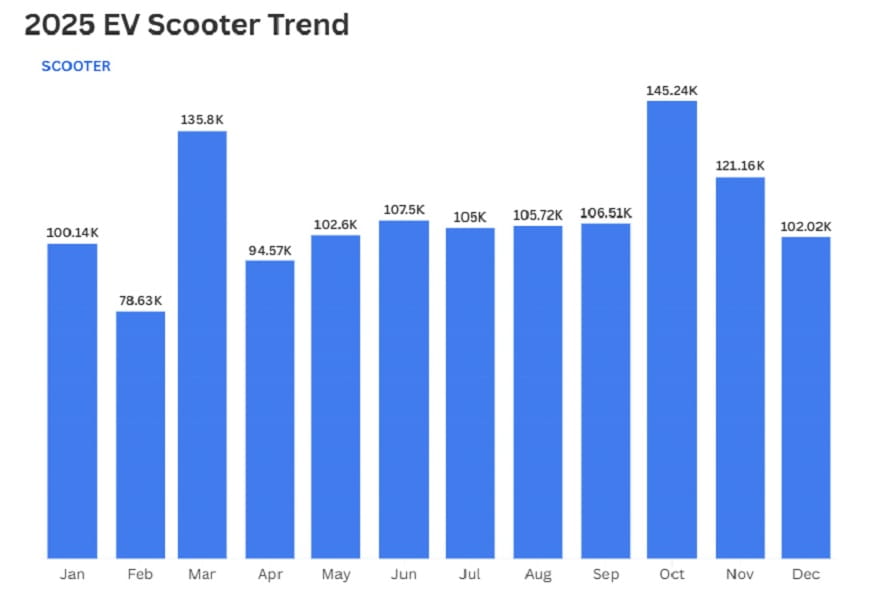

In 2025, India’s electric two-wheeler market is predominantly driven by scooters, which account for the majority of monthly volumes across the year. Scooter sales remain consistently strong, averaging around the 100k mark, with notable peaks during March and October, driven by festive demand and seasonal purchase cycles. This sustained momentum reflects high urban adoption, supported by affordability, ease of use, and suitability for daily commuting. The expanding charging infrastructure and increasing product availability further reinforce scooters as the backbone of EV adoption in India.

Electric motorcycles, while currently contributing lower volumes, show a gradual upward trend, particularly from mid-year to October. This growth indicates rising consumer interest in performance-oriented EVs and evolving market acceptance. Overall, the market reflects a clear structure-scooters leading large-scale adoption, while motorcycles emerge as a developing segment with strong future growth potential.

| MONTH | MOTORCYCLE | SCOOTER |

|---|---|---|

| JAN | 1.41k | 100.14k |

| FEB | 1.07k | 78.63k |

| MAR | 1.78k | 135.8k |

| APR | 1.11k | 94.57k |

| MAY | 1.35k | 102.6k |

| JUN | 2.39k | 107.5k |

| JUL | 2.53k | 105k |

| AUG | 3.23k | 105.72k |

| SEP | 2.5k | 106.51k |

| OCT | 4.3k | 145.24k |

| NOV | 2.29k | 121.16k |

| DEC | 1.73k | 102.02k |

India EV Two-Wheeler Market Leaders – 2025

In 2025, India’s EV two-wheeler market is strongly scooter-driven, with top models like TVS iQube, Bajaj Chetak, Ola S1, and Ather Rizta leading in volumes. This dominance is driven by high urban demand, affordability, ease of use, and a rapidly expanding charging ecosystem, positioning scooters as the core growth driver of EV adoption across the country.

Electric motorcycles, led by Revolt RV and Ola Roadster, remain a relatively niche segment with lower volumes, primarily driven by performance-focused and early-adopter consumers. However, the presence of emerging players indicates growing market interest. Overall, the market reflects a clear trend—scalable, mass adoption in scooters, alongside a gradually evolving motorcycle segment with long-term potential.

| MOTORCYCLE TOP 5 MODELS | 2025 VOLUMES |

|---|---|

| REVOLT: RV | 11.24k |

| OLA: ROADSTER | 9.11k |

| OBEN: RORR | 3.22k |

| ULTRAVIOLETTE: F77 | 1.15k |

| ULTRAVIOLETTE: X47 | 0.41k |

| SCOOTER TOP 5 MODELS | 2025 VOLUMES |

|---|---|

| TVS: IQUBE | 305.55k |

| BAJAJ: CHETAK | 279.54k |

| OLA: S1 | 195.86k |

| ATHER: RIZTA | 159.62k |

| ATHER: 450 | 57.32k |

EV Battery Trends: Efficiency in Scooters, Performance in Motorcycles

In 2025, India’s EV two-wheeler market reflects a clear divergence in battery capacity preferences between scooters and motorcycles. Scooter demand is heavily concentrated in the 2-4 kWh range, with 3-4 kWh alone contributing over 50% of the market. This highlights a strong consumer focus on cost-efficiency, optimal range, and practicality for daily urban commuting. Lower and higher capacity segments remain niche, reinforcing the dominance of mid-range configurations in driving mass adoption.

In contrast, the electric motorcycle segment is more performance-oriented, with 3-5 kWh batteries dominating the market. A significant share also extends into higher capacity ranges, indicating demand for longer range and enhanced performance. This trend reflects the evolving use case of motorcycles for extended travel and speed-driven applications. Overall, the market showcases a dual dynamic-efficiency-led growth in scooters and range-performance driven adoption in motorcycles.

Motorcycle-Battery Capacity Wise Market Analysis

| BATTERY CAPACITY | MOTORCYCLE MARKET SHARE |

|---|---|

| 3-4 KWH | 50.09% |

| 4-5 KWH | 40.79% |

| 10-11 KWH | 3.20% |

| 7-8 KWH | 2.86% |

| 2-3 KWH | 2.52% |

| 9-10 KWH | 0.55% |

Scooter-Battery Capacity Wise Market Analysis

| BATTERY CAPACITY | SCOOTER MARKET SHARE |

|---|---|

| 3-4 KWH | 51.71% |

| 2-3 KWH | 32.86% |

| 4-5 KWH | 12.74% |

| 1-2 KWH | 1.40% |

| 5-6 KWH | 1.28% |

| 7-8 KWH | 0.01% |